The Plan

The PRA Plan transitions Social Security to a system of individually owned, inheritable accounts that grow with wages. Workers under 55 receive retroactive credits and build PRA balances that yield higher benefits and greater flexibility than today’s system. As legacy retirees decline, FICA gradually converts into mandatory PRA contributions, ultimately creating a fully private, property-based retirement system with rising take-home pay.

Personal Retirement Accounts: Transitioning Social Security to Solvency

The Plan

Purpose and Governing Principle

This Plan replaces the Old-Age and Survivors Insurance (OASI) component of Social Security with a fully funded system of individually owned Personal Retirement Accounts (PRAs). The objective is permanent solvency, transparent financing, and individual ownership, achieved without federal borrowing, without general revenue transfers, without benefit provision, and without any mid-transition payable-benefits event. All operational rules, triggers, stabilizers, and timing conventions are governed by the Technical Specifications for Scoring, which control actuarial and budget evaluation.

Scope of Reform

The reform applies exclusively to OASI. Disability Insurance, Medicare, and other federal programs remain unchanged. Workers age 55 and older at implementation remain permanently in the legacy Social Security system. Workers under age 55 cease accruing new legacy OASI benefits and instead participate in the PRA system under the rules defined here and in the Technical Specifications for Scoring.

Eligibility and Cohort Structure

Implementation is assumed to occur on January 1, 2028. Workers age 55 and older remain under current law for life. All legacy benefits already accrued are honored in full. Workers under age 55 enter the PRA system and accrue no additional legacy OASI benefits after implementation.

Earnings Measurement and Continuity

The Plan preserves the familiar 35-year highest indexed earnings framework used in current-law Social Security. Prior FICA-covered earnings are indexed to the Average Wage Index (AWI) following established SSA practice. This continuity ensures scoreability, transparency, and conceptual stability while transitioning to an ownership-based system.

PRA Accumulation Structure

Transition Phase

For workers under age 55, accrued legacy benefits are converted into actuarially neutral Notional PRA Credits calculated using current-law AIME and PIA methodology. These credits represent explicit, wage-indexed retirement claims replacing further legacy accruals. Notional credits are not marketable assets and do not authorize borrowing; they are statutory claims payable under defined cash-flow rules.

Steady-State Phase

As legacy obligations contract through demographic attrition, the system transitions to fully funded custodial PRA accounts. Contributions are deposited into privately owned accounts held outside government bookkeeping and invested in diversified capital markets. Any residual notional balances are amortized under defined payout rules without reopening payroll taxation or permitting borrowing.

Mandatory Contribution Mechanics

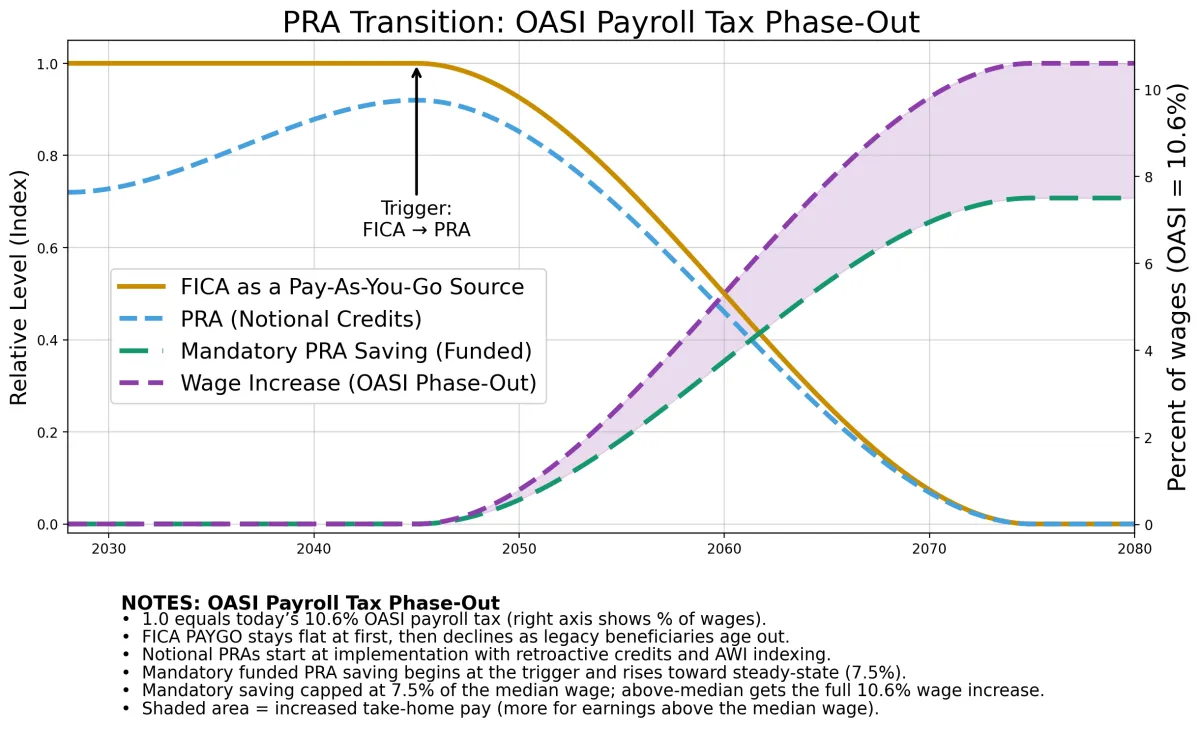

There are no add-on contributions at any stage. All funding derives exclusively from reclassification of the existing 10.6 percent OASI payroll tax.

In each year of transition, the funded PRA contribution rate equals the portion of the 10.6 percent OASI tax not required to finance remaining legacy OASI obligations in that year. If legacy costs require the full 10.6 percent, the funded rate is zero. As legacy costs decline, the funded rate rises automatically.

If required under high-cost assumptions, the funded rate may increase incrementally up to the full 10.6 percent statutory OASI rate. No payroll tax above 10.6 percent is permitted.

Mandatory contributions initially apply to earnings up to the national median covered wage. If high-cost solvency conditions require additional adjustment, the mandatory contribution base expands automatically toward the Social Security taxable maximum. This expansion operates mechanically and only if needed to maintain actuarial balance.

Voluntary Supplemental Contributions

Once the steady-state mandatory saving rate of 7.5 percent is reached, workers may voluntarily contribute additional amounts to their PRA accounts on earnings above the median wage and up to the Social Security taxable maximum. These contributions are tax-deferred, fully owned, and subject to the same custodial and payout rules as mandatory PRA savings. They are optional and create no government liability, but allow higher earners to replicate or exceed current-law replacement levels within the PRA framework.

Payroll Tax Phase-Out and Closure Gate

OASI payroll taxes remain in place during transition and are applied first to legacy obligations. PAYGO is considered closed only when two conditions are simultaneously satisfied:

1. The three-year moving average of remaining legacy OASI outlays falls below a statutory threshold in constant dollars; and

2. The Tail Coverage Ratio under high-cost certification satisfies the required solvency standard.

Only when both conditions are met does the OASI payroll tax permanently fall to zero. This dual-condition closure gate prevents premature elimination of payroll revenue and ensures orderly amortization of remaining obligations.

Tail Reserve and Solvency Discipline

A Tail Reserve accumulates excess payroll receipts during transition and is invested exclusively in Treasury obligations. The Tail Coverage Ratio measures the Reserve relative to projected notional payouts over a 30-year window. If the Coverage Ratio falls below required thresholds under intermediate or high-cost assumptions, automatic stabilizers activate.

Addressing the 2033 Funding Problem

The projected 2033 shortfall arises from a pay-as-you-go structure in which promised benefits exceed dedicated revenue. This Plan resolves that problem structurally by closing the legacy system to new accruals, maintaining payroll financing during transition, and embedding automatic stabilizers that prevent insolvency under high-cost assumptions. Scheduled benefits remain fully financed through deterministic reclassification and stabilization rules rather than across-the-board cuts or borrowing.

Stabilizer Structure

The Plan includes a closed, hierarchical stabilizer stack:

1. Funded-Rate Stabilizer – increases the funded contribution rate up to the 10.6 percent statutory ceiling if high-cost projections require.

2. Contribution-Base Stabilizer – expands the mandatory contribution base toward the taxable maximum if necessary.

3. Longevity Stabilizer – adjusts the Full Retirement Age prospectively if life expectancy materially exceeds projections.

These adjustments operate automatically and prospectively. Accrued principal is never reduced.

Retirement Age and Payout Rules

The Full Retirement Age is 68, phased in prospectively for affected cohorts. Early and delayed retirement adjustments are actuarially neutral. Funded PRA balances are converted to retirement income using life-only, inflation-indexed annuitization for baseline scoring. Alternative payout options may be modeled for sensitivity analysis.

Ownership and Inheritance

Funded PRA balances are owned property. Unannuitized balances pass to the worker’s estate. Notional credits during transition are treated as owned retirement claims subject to defined amortization rules.

Tax Treatment

Funded PRA contributions are tax-deferred for scoring purposes. Withdrawals are taxable unless otherwise specified by statute. Notional credits are treated as after-tax claims for ownership and inheritance purposes.

End State

In the end state, all workers participate exclusively in funded Personal Retirement Accounts. The OASI payroll tax is permanently eliminated once legacy obligations are extinguished and closure conditions satisfied. Government responsibility is limited to regulatory oversight. No residual federal retirement liability remains.

All technical assumptions, scoring parameters, and transition rules are governed by the Technical Specifications for Scoring.

This chart is illustrative and simplifies transition dynamics for visualization; it is not a precise actuarial projection. © 2025 PRAUSA

Summary of What the PRA Plan Achieves

• Replaces OASI with individually owned Personal Retirement Accounts.

• Protects all current retirees and workers age 55 and older.

• Resolves the projected 2033 funding shortfall structurally.

• Reduces the projected OASI open-group unfunded obligation, currently approximately $53 trillion under intermediate assumptions, by an estimated 60–70% immediately upon implementation.

• Converts accrued benefits for younger workers into actuarially neutral notional credits.

• Funds all retirement obligations without borrowing or add-on contributions.

• Reclassifies the existing 10.6 percent OASI payroll tax as legacy costs decline.

• Embeds automatic stabilizers that preserve solvency under high-cost assumptions.

• Establishes a fully funded steady-state system.

• Caps and, if necessary, expands the contribution base through defined rules rather than raising tax rates.

• Permanently eliminates the OASI payroll tax once legacy obligations are extinguished.

• Creates fully owned, inheritable retirement property held outside government bookkeeping.

• Replaces the pay-as-you-go system with a transparent, ownership-based retirement structure.

Social Security was built for a world that no longer exists. The PRA Plan replaces it in an orderly, transparent way that protects older Americans, empowers workers, strengthens families through inheritance, and restores long-run retirement solvency through ownership.

© 2026 All rights reserved. This document constitutes the original intellectual work product of Edwin Thompson. No portion of this document may be reproduced verbatim without attribution.

CALL TO ACTION

America will only secure real retirement freedom if millions of citizens demand it. Sign up to help push Congress toward action—and make this change a national priority.

© Copyright 2025. PRAUSA. All Rights Reserved. Content may not be reproduced without permission.

The Plan

The PRA Plan transitions Social Security to a system of individually owned, inheritable accounts that grow with wages. Workers under 55 receive retroactive credits and build PRA balances that yield higher benefits and greater flexibility than today’s system. As legacy retirees decline, FICA gradually converts into mandatory PRA contributions, ultimately creating a fully private, property-based retirement system with rising take-home pay.

Personal Retirement Accounts: Transitioning Social Security to Solvency

The Plan

Purpose and Governing Principle

This Plan replaces the Old-Age and Survivors Insurance (OASI) component of Social Security with a fully funded system of individually owned Personal Retirement Accounts (PRAs). The objective is permanent solvency, transparent financing, and individual ownership, achieved without federal borrowing, without general revenue transfers, without benefit provision, and without any mid-transition payable-benefits event. All operational rules, triggers, stabilizers, and timing conventions are governed by the Technical Specifications for Scoring, which control actuarial and budget evaluation.

Scope of Reform

The reform applies exclusively to OASI. Disability Insurance, Medicare, and other federal programs remain unchanged. Workers age 55 and older at implementation remain permanently in the legacy Social Security system. Workers under age 55 cease accruing new legacy OASI benefits and instead participate in the PRA system under the rules defined here and in the Technical Specifications for Scoring.

Eligibility and Cohort Structure

Implementation is assumed to occur on January 1, 2028. Workers age 55 and older remain under current law for life. All legacy benefits already accrued are honored in full. Workers under age 55 enter the PRA system and accrue no additional legacy OASI benefits after implementation.

Earnings Measurement and Continuity

The Plan preserves the familiar 35-year highest indexed earnings framework used in current-law Social Security. Prior FICA-covered earnings are indexed to the Average Wage Index (AWI) following established SSA practice. This continuity ensures scoreability, transparency, and conceptual stability while transitioning to an ownership-based system.

PRA Accumulation Structure

Transition Phase

For workers under age 55, accrued legacy benefits are converted into actuarially neutral Notional PRA Credits calculated using current-law AIME and PIA methodology. These credits represent explicit, wage-indexed retirement claims replacing further legacy accruals. Notional credits are not marketable assets and do not authorize borrowing; they are statutory claims payable under defined cash-flow rules.

Steady-State Phase

As legacy obligations contract through demographic attrition, the system transitions to fully funded custodial PRA accounts. Contributions are deposited into privately owned accounts held outside government bookkeeping and invested in diversified capital markets. Any residual notional balances are amortized under defined payout rules without reopening payroll taxation or permitting borrowing.

Mandatory Contribution Mechanics

There are no add-on contributions at any stage. All funding derives exclusively from reclassification of the existing 10.6 percent OASI payroll tax.

In each year of transition, the funded PRA contribution rate equals the portion of the 10.6 percent OASI tax not required to finance remaining legacy OASI obligations in that year. If legacy costs require the full 10.6 percent, the funded rate is zero. As legacy costs decline, the funded rate rises automatically.

If required under high-cost assumptions, the funded rate may increase incrementally up to the full 10.6 percent statutory OASI rate. No payroll tax above 10.6 percent is permitted.

Mandatory contributions initially apply to earnings up to the national median covered wage. If high-cost solvency conditions require additional adjustment, the mandatory contribution base expands automatically toward the Social Security taxable maximum. This expansion operates mechanically and only if needed to maintain actuarial balance.

Voluntary Supplemental Contributions

Once the steady-state mandatory saving rate of 7.5 percent is reached, workers may voluntarily contribute additional amounts to their PRA accounts on earnings above the median wage and up to the Social Security taxable maximum. These contributions are tax-deferred, fully owned, and subject to the same custodial and payout rules as mandatory PRA savings. They are optional and create no government liability, but allow higher earners to replicate or exceed current-law replacement levels within the PRA framework.

Payroll Tax Phase-Out and Closure Gate

OASI payroll taxes remain in place during transition and are applied first to legacy obligations. PAYGO is considered closed only when two conditions are simultaneously satisfied:

1. The three-year moving average of remaining legacy OASI outlays falls below a statutory threshold in constant dollars; and

2. The Tail Coverage Ratio under high-cost certification satisfies the required solvency standard.

Only when both conditions are met does the OASI payroll tax permanently fall to zero. This dual-condition closure gate prevents premature elimination of payroll revenue and ensures orderly amortization of remaining obligations.

Tail Reserve and Solvency Discipline

A Tail Reserve accumulates excess payroll receipts during transition and is invested exclusively in Treasury obligations. The Tail Coverage Ratio measures the Reserve relative to projected notional payouts over a 30-year window. If the Coverage Ratio falls below required thresholds under intermediate or high-cost assumptions, automatic stabilizers activate.

Addressing the 2033 Funding Problem

The projected 2033 shortfall arises from a pay-as-you-go structure in which promised benefits exceed dedicated revenue. This Plan resolves that problem structurally by closing the legacy system to new accruals, maintaining payroll financing during transition, and embedding automatic stabilizers that prevent insolvency under high-cost assumptions. Scheduled benefits remain fully financed through deterministic reclassification and stabilization rules rather than across-the-board cuts or borrowing.

Stabilizer Structure

The Plan includes a closed, hierarchical stabilizer stack:

1. Funded-Rate Stabilizer – increases the funded contribution rate up to the 10.6 percent statutory ceiling if high-cost projections require.

2. Contribution-Base Stabilizer – expands the mandatory contribution base toward the taxable maximum if necessary.

3. Longevity Stabilizer – adjusts the Full Retirement Age prospectively if life expectancy materially exceeds projections.

These adjustments operate automatically and prospectively. Accrued principal is never reduced.

Retirement Age and Payout Rules

The Full Retirement Age is 68, phased in prospectively for affected cohorts. Early and delayed retirement adjustments are actuarially neutral. Funded PRA balances are converted to retirement income using life-only, inflation-indexed annuitization for baseline scoring. Alternative payout options may be modeled for sensitivity analysis.

Ownership and Inheritance

Funded PRA balances are owned property. Unannuitized balances pass to the worker’s estate. Notional credits during transition are treated as owned retirement claims subject to defined amortization rules.

Tax Treatment

Funded PRA contributions are tax-deferred for scoring purposes. Withdrawals are taxable unless otherwise specified by statute. Notional credits are treated as after-tax claims for ownership and inheritance purposes.

End State

In the end state, all workers participate exclusively in funded Personal Retirement Accounts. The OASI payroll tax is permanently eliminated once legacy obligations are extinguished and closure conditions satisfied. Government responsibility is limited to regulatory oversight. No residual federal retirement liability remains.

All technical assumptions, scoring parameters, and transition rules are governed by the Technical Specifications for Scoring.

This chart is illustrative and simplifies transition dynamics for visualization; it is not a precise actuarial projection. © 2025 PRAUSA

Summary of What the PRA Plan Achieves

• Replaces OASI with individually owned Personal Retirement Accounts.

• Protects all current retirees and workers age 55 and older.

• Resolves the projected 2033 funding shortfall structurally.

• Reduces the projected OASI open-group unfunded obligation, currently approximately $53 trillion under intermediate assumptions, by an estimated 60–70% immediately upon implementation.

• Converts accrued benefits for younger workers into actuarially neutral notional credits.

• Funds all retirement obligations without borrowing or add-on contributions.

• Reclassifies the existing 10.6 percent OASI payroll tax as legacy costs decline.

• Embeds automatic stabilizers that preserve solvency under high-cost assumptions.

• Establishes a fully funded steady-state system.

• Caps and, if necessary, expands the contribution base through defined rules rather than raising tax rates.

• Permanently eliminates the OASI payroll tax once legacy obligations are extinguished.

• Creates fully owned, inheritable retirement property held outside government bookkeeping.

• Replaces the pay-as-you-go system with a transparent, ownership-based retirement structure.

Social Security was built for a world that no longer exists. The PRA Plan replaces it in an orderly, transparent way that protects older Americans, empowers workers, strengthens families through inheritance, and restores long-run retirement solvency through ownership.

CALL TO ACTION

America will only secure real retirement freedom if millions of citizens demand it. Sign up to help push Congress toward action—and make this change a national priority.

© Copyright 2025, PRAUSA. All Rights Reserved. Content may not be reproduced without permission.