Technical Specifications for Scoring

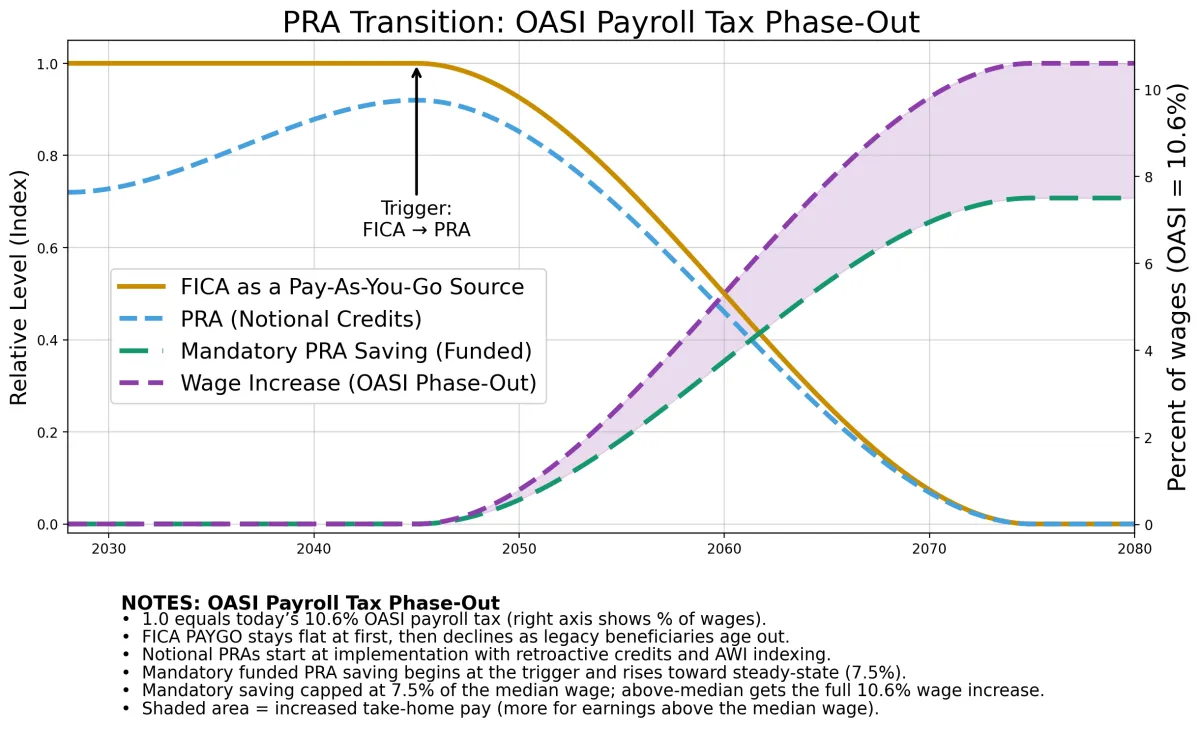

The PRA Plan transitions Social Security to a system of individually owned, inheritable accounts that grow with wages. Workers under 55 receive retroactive credits and build PRA balances that yield higher benefits and greater flexibility than today’s system. As legacy retirees decline, FICA gradually converts into mandatory PRA contributions, ultimately creating a fully private, property-based retirement system with rising take-home pay.

Technical Specifications for Scoring

The Technical Specifications for Scoring (TSS) provide the detailed actuarial framework required to evaluate the Personal Retirement Account Transition Plan under standard SSA Trustees methodology.

The document contains the formulas, cash-flow ordering rules, stabilizer triggers, indexing conventions, and closure conditions necessary for formal evaluation by the Office of the Chief Actuary (OCACT).

Because the TSS is written specifically for actuarial scoring and contains highly technical modeling detail, the full document is provided directly to actuaries and qualified reviewers engaged in formal evaluation.

High-Level Structure

Closed-group treatment of legacy OASI obligations

Immediate termination of new legacy accruals for workers under 55

Actuarially neutral conversion of accrued benefits

Mechanical reclassification of the existing 10.6% OASI payroll tax

Automatic high-cost stabilizers

Defined PAYGO closure gate and Tail Coverage requirements

Certification of zero borrowing in all projection years

The Plan is designed to stand or fall under formal actuarial scoring.

This chart is illustrative and simplifies transition dynamics for visualization; it is not a precise actuarial projection. © 2025 PRAUSA

CALL TO ACTION

America will only secure real retirement freedom if millions of citizens demand it. Sign up to help push Congress toward action—and make this change a national priority.

© Copyright 2025. PRAUSA. All Rights Reserved. Content may not be reproduced without permission.

Technical Specifications for Scoring

The PRA Plan replaces Social Security with individually owned, inheritable accounts that grow with wages. Workers under 55 receive retroactive credits and build PRA balances that yield higher benefits and greater flexibility than today’s system. As legacy retirees decline, FICA gradually converts into lower mandatory PRA contributions, ultimately creating a fully private, property-based retirement system with rising take-home pay.

Technical Specifications for Scoring

The Technical Specifications for Scoring (TSS) provide the detailed actuarial framework required to evaluate the Personal Retirement Account Transition Plan under standard SSA Trustees methodology.

The document contains the formulas, cash-flow ordering rules, stabilizer triggers, indexing conventions, and closure conditions necessary for formal evaluation by the Office of the Chief Actuary (OCACT).

Because the TSS is written specifically for actuarial scoring and contains highly technical modeling detail, the full document is provided directly to actuaries and qualified reviewers engaged in formal evaluation.

High-Level Structure

Closed-group treatment of legacy OASI obligations

Immediate termination of new legacy accruals for workers under 55

Actuarially neutral conversion of accrued benefits

Mechanical reclassification of the existing 10.6% OASI payroll tax

Automatic high-cost stabilizers

Defined PAYGO closure gate and Tail Coverage requirements

Certification of zero borrowing in all projection years

The Plan is designed to stand or fall under formal actuarial scoring.

This chart is illustrative and simplifies transition dynamics for visualization; it is not a precise actuarial projection. © 2025 PRAUSA

CALL TO ACTION

America will only secure real retirement freedom if millions of citizens demand it. Sign up to help push Congress toward action—and make this change a national priority.

© Copyright 2025, PRAUSA. All Rights Reserved. Content may not be reproduced without permission.